“Dear Ms Williams, The Digital Banking Unit of ACB Caribbean is seeking to confirm the validity of a transaction flagged within our systems using your International Debit Card ending ****. Kindly confirm whether this transaction was your attempt to make a purchase at the following: Merchant Name: WEIXIN*Beijing xxxx, Date: Oct 8, 2024 4:19:19 AM, Amount: $27.09/$9.98 USD. We look forward to hearing from you in this urgent matter by a response to this email or contacting us via telephone at 481 4399 to have a further discussion.”

My response “Thank you to the team at ACB for your diligence and protection. I did attempt the transaction, but it did not go through. I subsequently made the payment via another method. Thank you for the added layer of protection and I look forward to being able to continue to utilise the card with your usual level of diligence. Absolutely no complaints from me.”

Conversations like the one above have become an occasional but value-added part of my shopping experience during my four-month tour of China. This is not just from my preferred backing partner but also from my backup, usually via text, indicating ‘declined, transaction review,’ requiring a quick dash to email to confirm it was me, a resolution, and back to spending.

Attention to alerts like those in China is essential because digital payments are the primary regular transaction.

I had been prepared before arrival, well, sort of! My nephew from another mother had armed my phone with WeChat and AliPay and given me an overview of use. He omitted how dominant and practically essential my phone would become to my overall experience: to dine, to lime (go out), to communicate, for transportation, for necessities, and even to purchase from the street vendor.

Now, the mobile-to-pay experience was familiar to me. I have upgraded from Google-wallet to Apple-wallet and used for transactions in the US and the Caribbean, complements my new director of Petra affairs, my son. I strolled into the subway in New York, shopped, and dined without a care for cash, all from the comfort of my phone. While in Barbados earlier this year, I was able to have a similar experience at many of the restaurants but would occasionally have to dig out my wallet for the card and would have to grab cash for the street vendors.

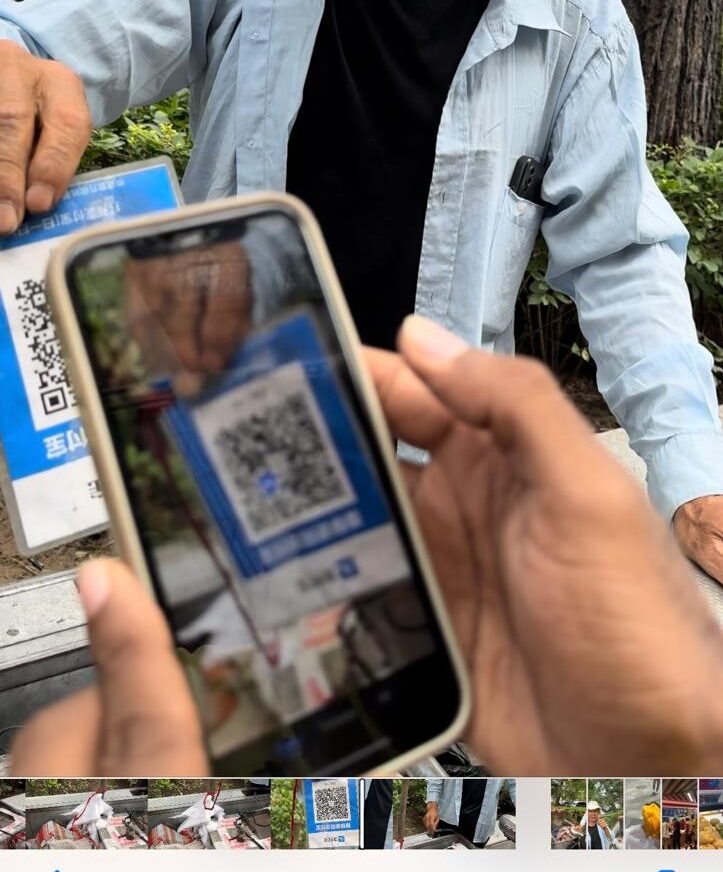

China has taken this mobile-to-pay to the next level. WeChat, a single app, does everything. One can load cash directly into Wexin Pay in WeChat from your bank account, or someone can transfer some money to you. You can also utilise the more-known option of loading your debit or credit card. It stores identification information, facilitates direct communication with vendors, allows access to sales and specials from your favourite stores, restaurants and entertainment providers, facilitates searches for anything you require, and converts from Chinese to the language you choose once you get the hang of it. It also performs the functions of Facebook, WhatsApp, Instagram… you get the idea. There is a supplemental option, Alipay, that facilitates transactions with the bonus of discounts and other deals just for signing in daily.

China is not cashless! One can choose to walk around with cash. There are ATMs every block and you can withdraw cash. All the Provinces I have visited to date are low risk for incidences of theft of bags, purses. And on occasions, I have seen the option of cash used, the cash was always accepted, with the stress and added time of getting change where required.

However, think on the convenience, we are already practically attached to our phones, so open and point or scan and go. And yes, for spending above certain amounts you must enter your passcode. And while using your international card, spending above a certain amount attracts a foreign exchange fee.

And WeChat or Alipay is accepted everywhere!! Purchasing roast sweet potatoes from the street vendor, getting my fresh pomegranate juice for my now Chinese vending buddy, using the public transport system, paying for my bullet train ticket in advance, going to the movies, general shopping, you get the picture.

With the fulsome digitisation, my appreciate for ACB Caribbean’s steady fraud management is welcomed. Ensuring I am protected even with a 12-hour differential and restoring full access the two times they have acted in my best interest and suspended use until I responded as advised.

My China adventures continue! Cashless, cardless, no wallet!! Me and my phone, my transactions central, a one stop point and go to pay for everything while keeping an eye for messages from my indigenous bank, ACB Caribbean contributing to my unforgettable China spectating experience.

I am ready to move beyond pulling my credit/debit card, peer transfer and EFT options for a single mobile-linked option in the shortest possible time when I return home. Let’s raise our game in this increasing fast pace technological, less-cash, global financial community.

PS – The inclusion of ACB Caribbean is my personal review and not a paid or solicited request from the institution